Dubai Logistics / Warehousing

Urban logistics income with a real scarcity premium behind it.

A six-unit premium warehouse development built around the segment of the Dubai logistics market that is hardest to replace quickly: well-located, mid-sized, high-quality space serving last-mile, 3PL, and light industrial occupiers.

Institutional-grade occupancy remains near 95% while prime Dubai industrial/logistics rents rose about 18% year-on-year. The project is underwriting into a market where useful space is scarce before the story even gets to exit upside.

Market references include Cushman & Wakefield Core H1/Q3 2025 marketbeats, Knight Frank UAE Industrial & Logistics Review 2025/26, and EZDubai/Euromonitor 2024-2029 e-commerce growth data.Why this segment, why now

Investors are not buying a warehouse. They are buying constrained urban logistics capacity with rising replacement value.

The key message is not abstract market growth. It is that demand from 3PL, e-commerce, and flexible occupiers is colliding with limited high-quality stock in the most useful submarkets.

Al Quoz and similar central submarkets capture premium pricing because operators are paying for delivery speed, visibility, and urban proximity, not just storage volume.

Current demand is not just speculative expansion. It is driven by logistics operators, e-commerce fulfillment, traders, and light industrial users who need speed-to-market and flexible footprint sizing.

New supply is arriving in outer corridors, but central last-mile product remains more capacity-constrained and more expensive, which supports rent resilience even if outer-submarket growth cools.

Project snapshot

A modular six-warehouse format aligned with what the market is actively leasing today.

Investor capital covers land acquisition and construction.

Capture demand from tenants priced out of scarce central stock.

Target recurring income before exit or phased sell-down.

Sell stabilized income, or break up units depending on buyer appetite.

Knight Frank says 58.1% of Dubai's 2025 requirements were concentrated in the 10,000–50,000 sq ft band. That makes a 1,000 m² module strategically intelligent: small enough for flexibility, large enough for serious occupiers, and easier to lease or dispose of than a monolithic single-tenant box.

Planning

The planning material makes the physical product visible, not just the financial story.

Site organization and circulation logic redrawn as a clean vector site-planning diagram for investor review.

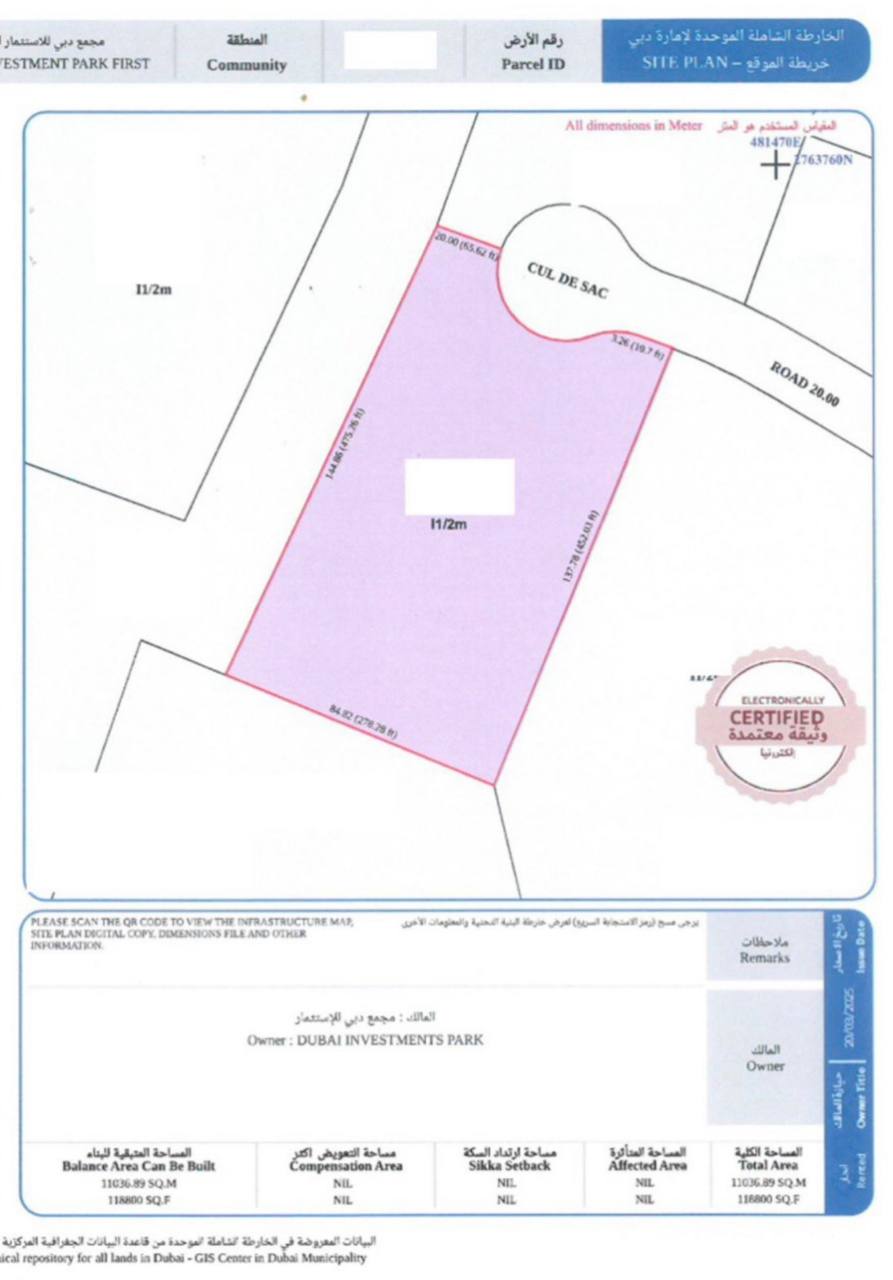

Parcel-level site plan showing land geometry, cul-de-sac access, road edge, and buildable envelope.

Economics at a glance

The deal already works on cash yield. The upside comes from scarcity, rent growth, and exit optionality.

Base underwriting assumes $13.6M investment, $1.587M gross income, 20% opex, and 9.34% net ROI at stabilization.

A roughly 9.3% stabilized net return is meaningful before adding upside from rent growth, scarcity premium, or exit compression.

If central rents continue rising while availability remains tight, NOI expands faster than in a commoditized outer-corridor warehouse product.

The project can be sold as yield or partially monetized as individual units, creating multiple exit paths rather than one narrow terminal event.

Market deep dive

Dubai logistics is benefiting from three overlapping forces: trade, e-commerce, and institutionalization.

UAE logistics remains structurally advantaged by its role between Asia, Africa, and Europe, plus infrastructure around ports, airports, free zones, and multimodal corridors.

EZDubai / Euromonitor estimate UAE e-commerce reached AED 32.3B in 2024 and may exceed AED 50.6B by 2029, reinforcing demand for fast urban fulfillment.

Occupiers are shifting from lower-quality stock into flexible Grade A assets, which supports higher rents, stronger pre-leasing, and investor appetite.

This is not an empty “Dubai growth” story. The segment has a clear supply-demand imbalance with real rent expansion already visible in data.

New supply may moderate some outer-submarket growth, but central proximity product can still hold a premium because it solves time-to-customer more than pure storage capacity.

Knight Frank's 2026 framing is important: performance is increasingly determined at the asset level by location, specification, tenant quality, and active management. That is supportive of a smaller, sharper product rather than generic bulk stock.

Exit logic

Two monetization paths reduce dependence on a single market outcome.

This route works if market appetite for stabilized logistics yield remains strong. Knight Frank notes prime-yield pressure moving toward sub-8% territory, which is directionally supportive for capital values if leasing is executed well.

This route matters because it expands the buyer universe and allows monetization even if institutional portfolio bids are slower than expected. Modular product is easier to distribute across smaller buyer pools than a single large asset.

Exit flexibility is one of the strongest features of the project. It gives the investor a way to monetize either as recurring yield or as modular product, which is a meaningful hedge against future market timing risk.

Risks and mitigants

The opportunity is attractive, but this is still execution-heavy real estate. Risk discipline matters.

Potential overruns and delays. Mitigation: fixed-price packages where possible, experienced contractors, milestone controls, contingency discipline.

If supply lands faster than expected, rent growth can cool. Mitigation: central positioning, modular units, target occupier diversity, early pre-leasing.

Yield buyers may demand higher cap rates. Mitigation: preserve break-up sale optionality and avoid relying on one terminal buyer class.

Confirm entitlement status, zoning fit, infrastructure access, and site-readiness before final close.

Re-underwrite with overruns, slower lease-up, and moderated exit pricing.

The investment case combines segment tailwinds with execution leverage. The quality of the opportunity will ultimately be defined by delivery discipline, tenanting strategy, and sponsor control.

Why an investor would lean in

Time-efficient decision case: attractive base yield, scarcity-backed segment, and more than one way out.

The fastest way to sell this deal is not to oversell the market. It is to show that the downside is understood, the base case is already respectable, and the upside is amplified by a structurally tight segment rather than by heroic assumptions.

Market references

Industry research supporting the investment case.

UAE Logistics & Industrial Market Update 2025/2026: Grade A occupancy ~95%, Dubai rents +18% YoY, >7M sq ft in pipeline.

cushwake.ae/en/insights/uae-logistics-industrial-market-update-20252026Dubai Industrial Q2 2025: warehousing rents +14% YoY in H1 2025.

cushwake.ae/en/marketbeats/dubais-industrial-and-warehousing-rents-climb-14-yoy-in-h1-2025Dubai Industrial Q3 2025: Al Quoz premium pricing, industrial/logistics rents +18% YoY.

cushwake.ae/en/marketbeats/marketbeat-industrial-q3-2025-dubai-uaeUAE Industrial and Logistics Report 2025/26: high occupancy, continued rental growth, 6.6M sq ft of supply due in Dubai in 2026, and 58.1% of 2025 requirements concentrated in the 10,000–50,000 sq ft band.

knightfrank.ae/newsroom/article/2026/2/the-uae-industrial-and-logistics-report-h2-2025UAE e-commerce market: AED 32.3B in 2024, expected to exceed AED 50.6B by 2029.

logisticsgulf.com/2025/05/uaes-total-e-commerce-market-is-expected-to-exceed-aed-50-6bn-by-2029/Contacts

Innovating for a greener future.

For investment materials, underwriting details, and next-step discussions, contact the team directly.

INVESTMENTS